Maine: Preliminary 2027 unsubsidized ACA rate changes: Indy market up 16.8%, sm. group up 15.7%; Manding/Taro out

Wed, 06/10/2026 - 4:55pm

via the Maine Dept. of Professional & Financial Regulation, Bureau of Insurance:

Mending Health Notifies Maine Bureau of Insurance that it Will Cease Offering Health Insurance Plans

AUGUSTA, ME – Mending Health, formerly known as Taro Health, has notified the Maine Bureau of Insurance that it will no longer offer health insurance as of January 1, 2027.

Mending Health’s approximately 1,100 members will keep their health plans through the end of their existing plan year.

Individuals/families who obtained Mending coverage through CoverME.gov, or who purchased a plan directly from Mending Health, can select a new plan with another health insurance company during the annual open enrollment period beginning November 1, 2026. New coverage will take effect January 1, 2027.

Small employer groups currently insured through Mending Health will also remain covered through the end of their plan year. As renewal dates approach, employers are encouraged to work with their insurance broker or agent to explore options with other insurers.

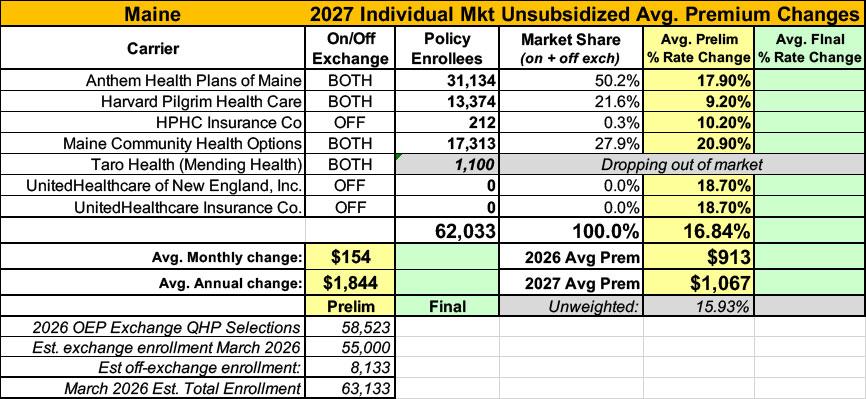

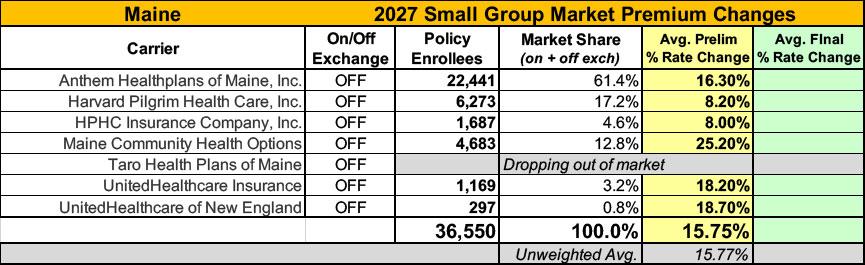

In Maine’s market for individuals/families and for small employer groups, four insurers submitted proposed rates to the Bureau of Insurance on June 5th for 2027 coverage: Anthem Health, Community Health Options, Harvard Pilgrim Health Care, and UnitedHealthcare. The Bureau is currently reviewing the proposed rates, which are expected to be finalized in August.

... Selective lapsation is expected to increase morbidity of the risk pool as a disproportionate number of healthy enrollees is expected to leave the market due to increases in their net premiums after subsidies and economic considerations. The cumulative morbidity factor can be found in Exhibit E, which is a factor of 1.0679 applied to claims.

Mending/Taro makes up less than 2% of Maine's individual market. I'm not sure how many small group enrollees they have.

Maine has also posted a summary table of the preliminary rate filings for the remaining carriers in both markets, which I've reformatted below as usual. Overall, individual market carriers are seeking average rate hikes of around 16.8%, while small group carriers are asking for 15.8% increases.

ANTHEM HEALTH PLANS OF MAINE:

Anthem Health Plans of Maine has made an application to the Maine Bureau of Insurance for premium rate changes for its fully ACA-compliant individual health plan products. This increase will impact approximately 31,134 Maine insured members renewing on 1/1/2027 with Anthem Health Plans of Maine. At the individual plan level, rate increases range from 9.0% to 26.2%. A subscriber’s actual rate could be higher or lower depending on the geographic location, age characteristics, dependent coverage and other factors. We expect some individuals will have an increase over 15%.

The primary drivers of premium increases are associated with increased cost of benefit expense for this ACA compliant block and the changes in the regulatory requirements. Increased cost of benefit expense is driven by increases in the price of services primarily from hospitals, physicians and pharmacies, coupled with members increasing their use of health care services, also called “utilization”. Increases in the price of services are driven by technological advances, new specialty medications, and a variety of other factors.

Increased utilization is driven by member level utilization and selection patterns in the Guaranteed Issue, Community Rated ACA market. Rates are in accordance with the regulatory framework and insurer participation in the market as of June 5, 2026. To the extent emerging data, changes to practice patterns that are impacting costs significantly different than assumed or if there are changes in regulation or insurer participation, then these rates may no longer be appropriate and will be evaluated for resubmission.

Harvard Pilgrim Health Care, Inc

Harvard Pilgrim is filing updated plans for 2027 to comply with the 2027 Clear Choice Designs published by the Bureau of Insurance in accordance with Rule 851. The existing 2026 enrollees have been mapped to the most similar 2027 plan in considering the rate increases for 2027. With these changes the increases by plan will vary, with some plans receiving higher increases and some receiving lower increases than the average. The average increase for renewing members is 9.2%.

The primary drivers of the rate increase include:

- Medical and pharmacy cost trend reflecting anticipated increases in unit cost, utilization, and service mix

- Difference in actual to projected experience

- Impact of the enhanced advanced premium tax credits (APTCs) set to expire after 2025

- Changes in benefit design and product mix

- Anticipated changes in risk adjustment

- Changes in administrative expenses

HPHC:

Harvard Pilgrim is filing updated plans for 2027 to comply with the 2027 Clear Choice Designs published by the Bureau of Insurance in accordance with Rule 851. The existing 2026 enrollees have been mapped to the most similar 2027 plan in considering the rate increases for 2027. With these changes the increases by plan will vary, with some plans receiving higher increases and some receiving lower increases than the average. The average increase for renewing members is 10.2%.

The primary drivers of the rate increase include:

- Medical and pharmacy cost trend reflecting anticipated increases in unit cost, utilization, and service mix

- Difference in actual to projected experience

- Impact of the enhanced advanced premium tax credits (APTCs) set to expire after 2025

- Changes in benefit design and product mix

- Anticipated changes in risk adjustment

- Changes in administrative expenses

Maine Community Health Options:

This rate submission is for PPO and HMO products that will be available for sale or renewal to individuals in the state of Maine during 2027.

Rule 856 required the individual and small group markets to be merged to form a single combined risk pool beginning January 1, 2023. The individual rates presented in this filing are developed based on the combined 2025 individual and small group experience.

The proposed rate changes for renewing plans offered to individuals in 2027 range from 13.3% to 34.8%. These average rate changes are calculated based on the current enrollment mix by area for each plan; actual rate changes will vary by rating area because of the change in rating area factors in 2027. The average rate change for renewing plans in this filing is 20.9%.

As of April 1, 2026 CHO had 16,513 individual members. CHO expects that its individual enrollment during 2027 will be 17,313 members.

...A rate change is needed to account for medical trend, as well as the following items:

- Expected marketplace morbidity changes caused by a shifting risk pool for certain populations purchasing exchange coverage after expiration of the enhanced federal subsidies, as well as the continued contraction of the small group market

- Development of underlying experience relative to expected

- Changes to plan benefit designs in 2027, including the changes to Clear Choice plans prescribed by the Maine Bureau of Insurance (BOI)

- Changes to the Maine Guaranteed Access Reinsurance Association (MGARA) 1332 waiver reinsurance program parameters in 2027

- Projected risk adjustment transfer payments

- Projected distribution of members by demographic category, geographic location, and plan

- Projected administrative expenses, taxes and fees, and profit

- Updated rating area factors

United Healthcare Insurance Company

The requested average rate change for the POS small group health benefit plans sold in the state of Maine is 18.2%, though rate changes may range from 11.8% to +25.8% depending on the specific plan. Additional premium changes may occur due to member aging and changes in plan selection. Rate changes will be effective January 1, 2027. It is projected that there will be 1,169 covered lives impacted by this rate change.

There are many different health care cost trends that contribute to increases in the overall U.S. health care spending each year. These trend factors affect health insurance premiums, which can mean a premium rate increase to cover costs. Some of the key health care cost trends that have

affected this year’s rate actions include:

- Increasing Cost of Medical Services: Annual increases in reimbursement rates to health care providers – such as hospitals, doctors, and pharmaceutical companies.

- Increased Utilization: The number of office visits and other services continues to grow. In addition, total health care spending will vary by the intensity of care and use of different types of health services. The price of care can be affected by the use of expensive procedures such as surgery versus simply monitoring or providing medications.

- Higher Costs from Deductible Leveraging: Health care costs continue to rise every year. If deductibles and copayments remain the same, a greater percentage of health care costs need to be covered by health insurance premiums each year.

- Cost shifting from the public to the private sector: Reimbursements from the Center for Medicare and Medicaid Services (CMS) to hospitals do not generally cover the cost of providing care to these patients. Hospitals generally make up this reimbursement shortfall by charging private health plans more.

- Impact of New Technology: Improvements to medical technology and clinical practice often result in the use of more expensive services - leading to increased health care spending and utilization.

Advertisement